- Home

- Bookkeeping Basics

- End of Year Bookkeeping

end of year bookkeeping

10 End of year bookkeeping tips

These 10 end of year bookkeeping tips will help you get your small business records up-to-date for the whole financial year, with the goal of being able to calculate your income tax obligations accurately.

Whether you use a Tax Accountant* or file your own self-employed taxes, you can work through these tips and checks.

*At the end of the financial year, your Accountant will probably give you a list of things they require you to do and any documents you need to gather for them to see, but if they haven’t done so yet you can use this page as a guide of what to start on.

Hint: Most of these tips can be handled on a monthly basis so that by year-end there isn't much work left to do.

Click above button to get our most popular Excel Template for easy bookkeeping! It's free.

1. When to do these end of year checks

A fiscal year is 12 months long. Your business operates for 12 months and then the accounts must be closed, financial statements prepared and tax returns filed.

The best time to do these end of year bookkeeping procedures and checks is shortly after you have closed off month 12.

For example, let’s say your financial year runs from January 1 2020 to December 31 2020.

It is likely that in January 2021 you will reconcile and close off your accounts for December 2020.

Once those December month-end procedures are finished, you can move onto these year-end procedures.

It is possible that you did not do much or any bookkeeping through the year and are just getting everything ready now so you can file your tax returns.

Whatever stage you are up to, read on to find out what must be done.

2. Process bank reconciliations

One of the first checks for end of year bookkeeping is to get your business bank reconciliations completely up-to-date.

By “up-to-date” I mean that your full 12 months has been reconciled and the closing balances in your accounts match, or reconcile to, the bank statements closing balances.

Now this is only going to work if you have a bank account for your business that is separate from your personal bank account – if for some reason you don’t then the approach is different and I discuss this in point 4. below.

It is always much easier to do the bank reconciliations once a month every month so that it is not such a big task at the end of the year.

What to do if you did no reconciliations

If reconciling your business bank account/s is something you didn’t do because you didn’t know or figured it would be fine for year-end, don’t worry.

Stop what you are doing now and go directly to your calendar and mark in a monthly time-slot for each of the next 12 months to reconcile your accounts.

The end of year bookkeeping checks may take a little longer than you wanted but it’s important to get this right so that your taxes are right.

You are going to now set aside a few hours (or more depending on how many monthly transactions you have) and carefully work through the reconciliations, one month at a time.

Don’t move on to the next month until the month you are working on is reconciled.

I explain more on these pages what is involved in reconciling and how to actually do it step by step.

Bank Reconciliation Statements

Bank Reconciliation Step-by-Step Example

What other accounts must be reconciled

Here is a list of other accounts that should be reconciled for your end of year bookkeeping if you have them:

- Savings Account

- Petty Cash Box

- Paypal or Stripe (or similar)

- Credit Card

- Credit Line

- Loan Account

3. Bring in Expenses paid with personal money

If you have a business bank account in which all of your business transactions were entered, but you know you have paid for some business expenses out of your personal bank account and you haven’t entered them into your bookkeeping system yet, give them to your Accountant to sort out, or enter them now yourself...

...like this:

- Make a list of what they are and figure out the appropriate ledger account for each – if you have several expenses that can be grouped into one ledger account, then calculate their total.

- Next, prepare a journal to enter them into your books.

- The journal will be:

DR Expense (split them out to whatever account code is appropriate for each expense)

CR Capital (Owner's Equity) - Date the journal using the last day of the last month of your financial year.

Below is a visual example of a bank statement (only for one month) that has been highlighted to show business costs, and the second image is a journal for them.

End of Year Bookkeeping Tips: Personal Bank Statement Highlighted Business Expenses

End of Year Bookkeeping Tips: Personal Bank Statement Highlighted Business Expenses End of year bookkeeping journal: Expenses paid with personal money

End of year bookkeeping journal: Expenses paid with personal money4. reconcile personal bank account

Here I explain what to do if you don’t have a bank account for your business and so your personal bank account is a mixture of all your business and personal income and expenses.

This is different to if you took drawings from your business bank account or deposited personal money into it, so don’t get these two concepts mixed up.

The concept explained in this point is targeted towards people who started a business but didn’t open a separate bank account from their personal one to record business transactions.

how to do bookkeeping when all transactions are mixed inside your personal bank account

I recommend going through each monthly personal bank statement, highlight the business transactions (just like in Step 3. above but also including money from sales) and enter these into your bookkeeping system or spreadsheet as income or expenses.

If you are using bookkeeping software you can enter the transactions in through journals (see example in Point 3 above for the example journal).

You will need to also include income from sales that you deposited into your personal bank account. Below is a journal entry showing how to enter these income transactions.

DR Owner's Capital (Personal Deposits)

CR Income

If you are using spreadsheets your goal is to enter in all the Income into Income accounts and all the Expenses into expenses accounts.

You don't have to indicate individual dates for each transaction.

You can group all Income into one transaction for the month for Sales, and you could even group all Expenses into one transaction for the month for Expenses, however, I would prefer to split this one transaction out into separate expenses accounts.

Note: You will not need to keep a record of the bank balance or process an actual bank reconciliation for this method of bookkeeping otherwise you would have to enter all your personal income and expenses so that the bank reconciles, which is time consuming for no good reason.

However, if you do find you want or need to do it this way, there is a short-cut...

...group all personal expenses into one total for each month, and all personal deposits into one total for each month and calculate the difference.

Enter this difference into the bank screen of your software dated the last day of the month and code it to Owner's Drawings.

Then you can go ahead and enter all individually dated business income and expenses for each month through the bank screen of your software and reconcile your personal bank account (you will have to make sure you have entered the opening balance of your personal bank account into the bank ledger account at the start of the financial year).

5. Quick-check your ledger accounts

Check that each income and expense type has been entered to the correct ledger account throughout the year, and for the regular bills check they have been entered to the same ledger account consistently...

Check Detailed Ledger in bookkeeping software

...pull up a detailed general ledger report for your full tax year in your bookkeeping software and scroll down through it on-screen looking for any transaction that might have been entered to the wrong type of account. Don't be too fussy about it - this should just be a quick glance down through each account to see if anything 'jumps' out at you as being wrong.

See the example below which is an extract from Xero accounting software.

End of Year Bookkeeping Tips: General Ledger Checks

End of Year Bookkeeping Tips: General Ledger ChecksHint: A quick way to check for inconsistencies when processing end of year bookkeeping checks:

Using a phone bill as the example, does the cost of the phone bill show up regularly in your ledger expense account for the phone account every month? You can check this in either the detailed general ledger report, or in an Income Statement that displays every month side by side. If a month is missing a phone cost, perhaps it has been entered to the wrong ledger account; try to find it and then move it to the phone account.

Often the best way to make a correctional adjustment in the software is through journal entries – these move the amounts from one ledger account to another ledger account without affecting your bank account (which you have worked so hard to reconcile so you don’t want to mess it up now!).

Check accounts in bookkeeping spreadsheets

If you are using a simple cash book or bookkeeping spreadsheet opposed to bookkeeping software, when doing your end of year bookkeeping checks cast your eyes through the profit and loss report (if you have one) or through each month’s entries and make sure you are happy with the income and expense categories you have chosen for every transaction, and for consistency.

What if you don't know what account to use

If you are unsure what type of account some transactions are supposed to be entered to, please seek help from a bookkeeper.

Keep in mind that some transactions are not deductible business expenses so you must make sure they are not included in profit and loss type of accounts (from which income tax is calculated) – they must go on balance sheet accounts. This is important to avoid under-paying your income tax to the authorities.

If you use a Tax Accountant, you could post these types of transactions to a Balance Sheet account called Suspense so that you can get on with the rest of your tasks. It's a good place to hold an amount that needs to be dealt with sometime later as it doesn't affect your profit - but it will have to be sorted by the year-end. Ask your Accountant.

6. calculate your total outstanding debtors and creditors

In an accrual system any outstanding amounts must be included in the end of year bookkeeping calculations for tax purposes.

This is for outstanding sales invoices which your customers haven’t paid yet (receivables).

Or outstanding bills which you haven’t paid yet (payables).

Not every business has to pay tax on accrued amounts (such as in the USA only larger businesses must do this). Check up on where you live to find out your obligations.

If you are using full-featured bookkeeping software where you enter all your sales and purchase invoices, your system will enable you to quickly produce a report for the outstanding amounts.

However, if you haven’t entered invoices into your bookkeeping software you will need to manually compile a list of what’s outstanding.

what outstanding bills to include in end of year bookkeeping

If your balance date is 31 December and:

- you receive a bill in the post in January

- that is dated 31 December or earlier

- and you only pay for it in January or later

- it needs to go on the list.

how to handle old, unpaid purchase invoices

If you have old outstanding purchase invoices but you are sure they were paid, investigate why they are still showing and fix them in your system.

A classic error that many people make is to pay a vendor but instead of applying the payment to the invoice in the bookkeeping system, they've entered the payment directly to the expense account.

This actually means the amount will be showing twice in their expenses (once through the invoice, and once through this direct payment). If this is you, find out how to fix it in your bookkeeping software.

What Outstanding Sales Invoices to Include

Or, you might send an invoice to a customer dated 10 December, but they only pay you in January, this amount must go on the list.

Also include any other outstanding amounts, no matter how old (you might have some that are years old, but I hope not!).

how to handle old unpaid sales invoices

The same could apply to sales invoices where you received a payment but instead of applying the payment to the invoice, you’ve entered it directly to the income account.

These need to be fixed.

If your old customer invoices have not been paid, consider writing them off to bad debts (see Step 7 below).

7. Write-Off Bad Debts

The end of year bookkeeping checks is a good time to write off any debtor amounts that you don’t expect to receive payment for.

It could either be for a very small balance that’s not worth chasing the customer for, or the customer has moved away never to be heard from again but you have gone through the debt collection process to try and get the money to no avail.

The journal for writing off bad debts is this:

DR Bad Debts expense

CR Accounts receivable

Date it the last day of the fiscal year.

The advantage of writing off these with your end of year bookkeeping is to clear out those pesky small outstanding invoices that keep showing up on your list every month, and it reduces your profit thereby reducing how much income tax you must pay.

8. Count your stock

This end of year bookkeeping tips is for you if you buy and sell physical items that you keep in your own stock room.

Note: if you sell goods using the following methods, you will not be counting any stock because the inventory isn’t yours. The owner of the inventory will do the stock take for their own records:

- drop-shipping

- affiliate method

- consignment stock

A stock take should ideally be performed

A stock take should ideally be performed within the last month of the end of tax year and any necessary adjustments made in the bookkeeping system to align the inventory account to match the total value of items on hand.

The inventory balance should be shown at the cost price, that is, the price paid for it, not the price it is being sold for. Also, it should exclude sales tax.

If any stock is missing or broken the cost can be written-off to an expense account or cost of goods sold account.

Depending on where you live you may need to use the Fifo (first-in, first-out) or Lifo (Last-in, last-out) or Average cost method to calculate the amount of stock that you are writing off, as well as the value of stock you have on hand at the end of the tax year.

Here is an example by Wikihow for writing off stolen stock.

Your business needs to be closed on the day of stock-take so that no adjustments are made in the bookkeeping system whilst the count is happening!

9. Reconcile your payroll tax and sales tax

It's a good idea to check that the total amounts for these tax totals in your bookkeeping system for the year, match the total of what you have reported to the tax authorities for the year.

Or at least for the first 11 months because you might not have filed your 12th month returns yet when starting these end of year bookkeeping checks.

If there are any variations it means that you may have accidentally made some changes in your bookkeeping system since you filed your reports.

You must find out what has gone wrong and make the necessary adjustments to fix this.

Either, the changes are a mistake and the entries should have gone to a different ledger account, or your adjustments were not reported to the tax authorities which you must now look at doing with your end of year bookkeeping process - but do this with care because you may be charged penalties.

Speak to a professional bookkeeper if you are not sure what to do, or ask your Tax Accountant to help with this.

10. Depreciation

If your business has purchased assets through the year, you (or your Tax Accountant) will need to calculate the depreciation for the end of year bookkeeping and enter it into the records as an expense, thereby reducing your profit, thereby reducing how much tax you must pay to the government.

You can find out more about Depreciation on Assets here.

Get our most popular Excel Template for easy bookkeeping! It's free.

Site Sponsors

From The Blog

-

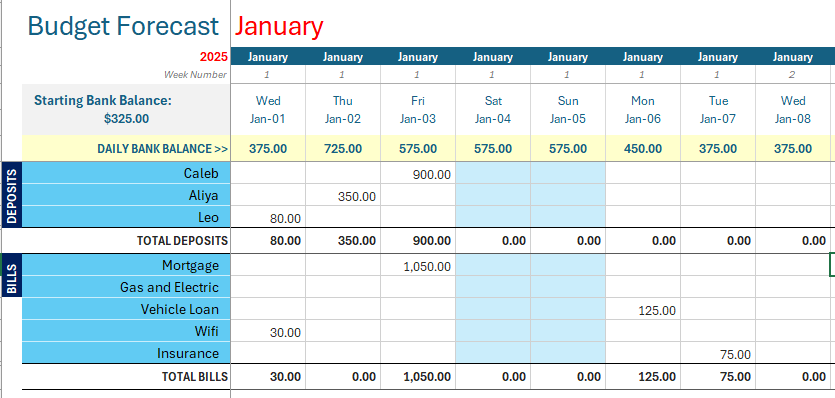

Budget Forecast Template Excel for 12 Months

Feb 27, 25 08:25 PM

Free Budget forecast template Excel for your bills for 12 months and ensure there is always enough money in your bank to pay your bills.

Free Budget forecast template Excel for your bills for 12 months and ensure there is always enough money in your bank to pay your bills. -

How is Sales Tax Calculated

Jul 25, 24 01:07 AM

How is sales tax calculated? The main formula is: the price multiplied by sales tax rate, see more formulas, lots of examples, get free Excel calculator.

How is sales tax calculated? The main formula is: the price multiplied by sales tax rate, see more formulas, lots of examples, get free Excel calculator. -

What is Sales Tax

Jun 05, 24 11:07 PM

What is sales tax? It is a consumer tax charged to customers and paid on to the government by the business making the sale. Technology can help automate this process.

{kind=link}

Facebook Comments

Leave me a comment in the box below.