- Home

- Double Entry Bookkeeping

Double Entry Bookkeeping

7 Step Guide to Processing Business Accounts

Double entry bookkeeping is where the value from every business transaction is entered twice into the system.

Learn the principles behind this system and your confidence will grow in leaps and bounds whether keeping the books manually or using software!

Click above button to get our most popular Excel Template for easy bookkeeping! It's free.

Understanding double entry bookkeeping will also help you get a better grasp of how Balance Sheets work.

the basic steps of double entry bookkeeping

- Business transactions produce documents.

- The information from the documents is recorded into journals.

- The data is taken from the journals and entered (posted) into ledgers.

- Each ledger contains various accounts, listed in the chart of accounts.

- These accounts are totaled and balanced in line with the accounting equation.

- The accounts are balanced by using debits and credits, which is the core foundation of double-entry bookkeeping.

- A trial balance can be produced to ensure that the books actually balance and that the debits and credits have been posted correctly.

- Finally Financial Statements are prepared

More details of each of these steps can be found below.

1. When a business carries out an activity a document is produced

One document example would be a sales invoice.

A business activity is the selling, buying, borrowing or loan of items, cash, goods or services.

For example: a sales invoice would be raised when the business sells a product.

The activity (in this case, a sale) is defined as a business transaction.

The document is called an accounting source document.

2. The transaction starts its journey in the Journal books

The most basic details of a business transaction can be found on the source document and include:-

- the date

- the name of person or company

- a description of the transaction

- the amount

These details are recorded into books of original entry commonly called day books or bookkeeping journals.

The journals describe in summary what the transaction was and what ledger accounts are affected.

A transaction that has no value attached would not be recorded in the accounts.

View examples of bookkeeping and accounting journals

Make your own journal examples with journal entry template in excel

3. next, the ledger accounts are updated

The amount or value of the transaction will be entered into the bookkeeping ledgers.

One ledger represents one account.

If there are a lot of transactions in that one account, one ledger might spread on to several pages.

Each ledger is laid out in a T format.

Depending on the type of account, the amount will be entered into either the left-hand side of the T, or the right-hand side of the T.

In double entry bookkeeping, there are always two accounts affected by one transaction amount to keep the books in balance.

Which leads us on to the debits and credits.

4. the amount is entered twice using a debit and a credit

The amount is entered to the general ledger accounts using the debits and credits method.

It is entered once as a debit in one account ledger, and once as a credit in another account ledger.

A bookkeeper needs to learn how to process debits and credits to ensure the ledger balances are accurate. There is a cheat sheet available to print.

It is not that difficult because there are only five main account categories within the ledgers, so only five to learn.

For example, one main ledger category is "expenses".

Expenses are always debited when money is spent on an expense.

The opposite credit entry will be made in the cash account (or bank account) which can be found in the "assets" ledger category.

Bookkeepers should know which accounts to debit and which accounts to credit.

5. Chart of Accounts

The names and numbers of all the ledger accounts are found in a list called the Chart of Accounts where they are created, maintained or archived.

All accounts come under five main category headings which either go on the Balance Sheet (for example Asset Accounts) or the Income Statement (for example Expenses).

These five main types of bookkeeping accounts are further classified into two groups, permanent or temporary which dictates which report they go on.

6. There is a mathematical formula to support double entry

It is called the accounting equation and it maintains the structure of the ledgers.

Learning this simple equation by heart can help a bookkeeper to remember the rules of debits and credits.

It is from the bookkeeping ledgers that the totals are totaled.

The trial balance is then produced.

7. a trial balance shows if the ledgers balance

The Trial Balance is used to ensure that all the debit ledger accounts add up to the same value as all the credit ledger accounts.

You can read more about the Trial Balance here.

If corrections must be made, this is the time to it and then a corrected trial balance produced.

A complete example from Journals to Reports

You can find a complete bookkeeping example here which shows the movement of two transactions (an income and an expense) going through the journals, ledgers and reports.

8. Financial statements are prepared

After the trial balance is completed, financial statements are prepared including an Income Statement and a Balance Sheet. These can be done once a month to help the business owner see how their business is performing.

A tax accountant will prepare specialized financial statements at the end of the financial year before calculating income tax to be paid; the steps involved in this preparation include:

- preparing adjusting entries for the year for accruals and deferrals

- preparing closing entries (moving temporary balances to the equity account)

- preparing an adjusted trial balance

There is another method of bookkeeping: single entry bookkeeping

This is basically just a cashbook.

Single entry is a good place to start for micro and small businesses.

It does not require using journals and ledgers or entering the amount of a transaction twice. It only has to be entered once.

Bookkeeping programs use the double-entry method

The way in which these programs are set up means you don’t really notice the double entry bookkeeping rules in action although they are very much in operation in the background.

The interface makes it easy to input basic data which is then immediately and automatically processed in a journal, placed into the correct ledger accounts, totaled and balanced.

You will be none the wiser on the whole method. So if you want to learn it, you need to do some manual practicing.

Take the quiz!

The business transaction for the quiz

On January 10th Peter buys $20 of stationery from Stationery Store. He pays with his business bank card and Stationery Store gives him a receipt.

Take the Quiz!

The business transaction for the quiz

On January 10th Peter buys $20 of stationery from Stationery Store. He pays with his business bank card and Stationery Store gives him a receipt.

Click on the button below to take the quiz.

Get our most popular Excel Template for easy bookkeeping! It's free.

Site Sponsors

From The Blog

-

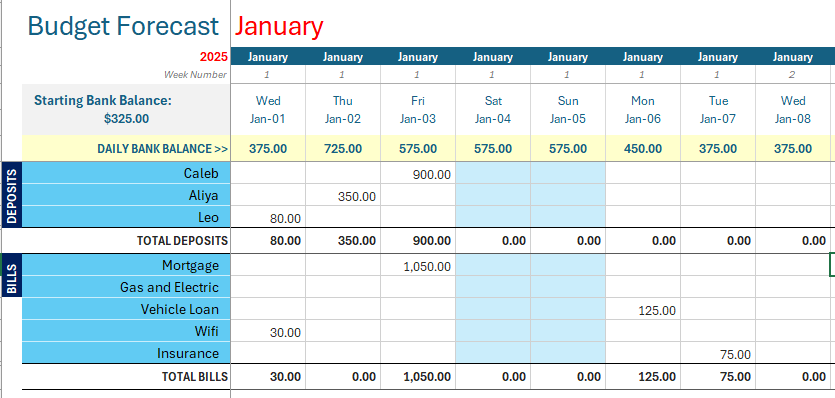

Budget Forecast Template Excel for 12 Months

Feb 27, 25 08:25 PM

Free Budget forecast template Excel for your bills for 12 months and ensure there is always enough money in your bank to pay your bills.

Free Budget forecast template Excel for your bills for 12 months and ensure there is always enough money in your bank to pay your bills. -

How is Sales Tax Calculated

Jul 25, 24 01:07 AM

How is sales tax calculated? The main formula is: the price multiplied by sales tax rate, see more formulas, lots of examples, get free Excel calculator.

How is sales tax calculated? The main formula is: the price multiplied by sales tax rate, see more formulas, lots of examples, get free Excel calculator. -

What is Sales Tax

Jun 05, 24 11:07 PM

What is sales tax? It is a consumer tax charged to customers and paid on to the government by the business making the sale. Technology can help automate this process.

{kind=link}

{kind=link}

Facebook Comments

Leave me a comment in the box below.