- Home

- Double Entry Bookkeeping

- Accounting Source Documents

Accounting Source Documents

The start of the bookkeeping process begins with accounting source documents - the paperwork.

In most cases, when a business transaction is carried out a document is produced which contains the details of each transaction.

These documents get their name from the fact that they are the origin of the information that is recorded into the accounting books.

Click above button to get our most popular Excel Template for easy bookkeeping! It's free.

Both businesses (or people) involved in the transaction will get a copy of the accounting source document produced.

The documents come in all sorts of shapes, sizes, colors and types of paper.

They can be on physical paper or electronic files like PDF.

Every document has a few things in common:-

- The transaction date

- The amount

- The name of both businesses/people

- A reference number

- A description of the transaction

Types of Accounting Source Documents

There are many different types of source documents.

Below is a list of ten that are used regularly by most businesses.

- Quotes

The buyer may require a quote from different sellers for the items it wants to buy.

The quotes will be looked at, discussed and a decision made as to which seller to buy the product from, usually based on who is the cheapest.

After that an order will be placed and the winning supplier will turn the quote into a sales invoice. - Orders

When a business needs to buy an item it will complete an order form.

The order form may be as simple as an A5 sheet from a duplicate book, or it may be a form supplied by the seller through its on-line website or catalogue.

Order forms will not always show the cost because the buyer may not know the cost when placing an order. - Delivery Dockets

In many cases the vendor will provide a delivery docket with the items being shipped, posted or delivered.

These will often have a description of items being delivered so the buyer can check it against their order immediately upon its arrival. - Sales and Purchase Invoices

When an item is sold the seller will issue a document providing all the details of the sale.

If the seller does not expect cash up front before sending the item, they will state on their invoice their payment terms i.e. the length of time the buyer has until it’s time to pay.

One example is for payment to be received no later than 30th of the month following the date of invoice.

The seller enters the document into their system as a sales invoice.The buyer will enter it into their system as a purchase invoice. - Credit and Debit Notes

If the buyer decides not to keep an item but return it to the seller, the seller will issue a special note to show the amount to be refunded.

In the supplier’s bookkeeping system this is called a credit note because it reduces the amount owed by the customer.

In the customer’s bookkeeping system it is called a debit note because it reduces how much they owe to the seller. - Payment/Remittance Advices

When a customer pays their bill they will send the supplier a remittance advice which details the amount and the invoice numbers being paid.

It will be posted either with the check or by itself if payment is made by internet banking.

Remittances can often be found already printed as a small cut out section at the bottom of, or down the right hand side of, the sales/purchase invoice. - Checks (Cheques)

A check (cheque) is a special bank note that represents the cash that is being paid by the customer.

The check requires the signature of the person who is an authorized signatory of the bank account from which the check is issued. Each check has a special number on it which should be recorded into the bookkeeping system.

The name of the payee should be written on the check. If it is left blank anyone can fill it in with their own name and deposit the check, thus stealing the money.

Checks should be crossed across the top with the words ‘not negotiable’, and the printed words ‘or bearer’ crossed off (not all checks have this) so that the check has to be deposited into the payee’s bank account and not cashed, thus avoiding theft. - Receipts

Once the customer has paid their bill, the supplier can issue a receipt.

A receipt is proof that the payment has been made, which is a good idea when paying cash.

Receipts are usually automatically provided when buying something from a shop. - Deposit Slip

When a customer pays by cheque or cash, the seller will write a bank deposit slip which will be taken to the bank and presented together with the cheques and cash.

The deposit slip will show the total amount being deposited plus a break-down of the cheque amounts and cash.

The bank will make a record of the payment so that it shows up on the payor’s bank statement as a payment received, and on the customer’s bank statement as a payment made. - Other

Accounting source documents may include loan or lease agreements with attached payment summaries that show the total amount due plus interest and administration fees.

Filing the Documents

It is vital that all accounting source documents are filed in such a way that they are easy to retrieve at a later date in case of any queries that might pop up.

The most common method is to file everything in date order, then alphabetical order.

Most tax departments will require you to maintain a

good office filing system for at least 5 or 7 years.

Common Terms/Words

- Payee - person or business being paid or receiving payment

- Payer - person making the payment or paying funds to another business or person

- Seller - supplier (payee)

- Buyer - purchaser; customer (payor)

Accounting Source Documents Quiz

Take the quiz and test your knowledge on what you have learned from this page.

Accounting Source Documents Quiz

Take the quiz and test your knowledge on what you have learned from this page.

Get our most popular Excel Template for easy bookkeeping! It's free.

Site Sponsors

From The Blog

-

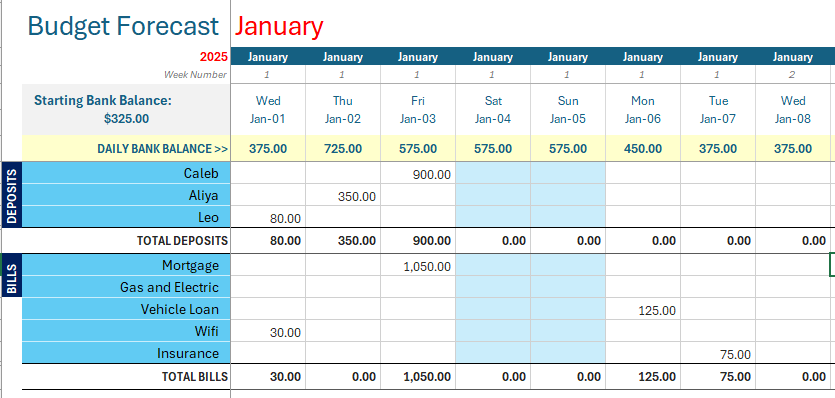

Budget Forecast Template Excel for 12 Months

Feb 27, 25 08:25 PM

Free Budget forecast template Excel for your bills for 12 months and ensure there is always enough money in your bank to pay your bills.

Free Budget forecast template Excel for your bills for 12 months and ensure there is always enough money in your bank to pay your bills. -

How is Sales Tax Calculated

Jul 25, 24 01:07 AM

How is sales tax calculated? The main formula is: the price multiplied by sales tax rate, see more formulas, lots of examples, get free Excel calculator.

How is sales tax calculated? The main formula is: the price multiplied by sales tax rate, see more formulas, lots of examples, get free Excel calculator. -

What is Sales Tax

Jun 05, 24 11:07 PM

What is sales tax? It is a consumer tax charged to customers and paid on to the government by the business making the sale. Technology can help automate this process.

{kind=link}

Facebook Comments

Leave me a comment in the box below.